Written By Roque M. Sorioso, Jr.

Corruption is a pervasive threat that devastates economic growth, undermines governance, and destroys public trust in the government. Yet, cutting-edge research in anti-corruption and asset recovery, analyzed through the powerful lenses of economics and law, unveils revolutionary insights essential for formulating and implementing potent anti-corruption policies. This article synthesizes the latest data and emerging trends, highlighting their significant policy implications for local governments, institutions, and agencies. By wholeheartedly embracing these insights, stakeholders can dramatically boost the effectiveness and fairness of anti-corruption strategies, forging a path toward a more equitable and thriving Philippines.

Foundations of Asset Recovery Economics

A discussion of the subject is not complete without a short survey of seminal works that paved the way for the shift from traditional punitive criminal justice models to more asset-focused approaches. Rose-Ackerman’s book, “Corruption and Government” (1999), for example, changed the perspective on corruption by framing it as a failure in governance systems. Pieth and Aiolfi (2004) introduced the concept of corporate responsibility into discussions on transnational corruption, significantly influencing OECD protocols. Stephenson (2011) went a step further by establishing a legal foundation for non-conviction-based asset forfeiture (NCBAF), which has led to reforms in countries such as Nigeria and Peru. The World Bank’s StAR Initiative has also conducted studies on the challenges of asset repatriation, highlighting the need for improved international cooperation. Together, these studies have steered the field towards a more multidisciplinary approach, blending elements of law, economics, valuation, and institutional design. They continue to be crucial in shaping policy discussions regarding legitimacy, efficiency, and political feasibility. However, this article will focus on the NCBAF, as there is an urgent need to focus on asset recovery rather than the drama that is the many attempts at criminal -but mainly political- punishment, the typical Philippine mechanism to fight corruption.

Applications

The NCBAF is a legal mechanism that allows governments to seize assets suspected of being linked to criminal activity, such as corruption, money laundering, or fraud, without requiring a criminal conviction. It is particularly useful under the following conditions: if the suspect is dead, missing, or has fled the Philippine jurisdiction; if the statute of limitations has expired; or if the suspect is immune from prosecution due to political office or diplomatic status.

Unlike traditional criminal forfeiture, the NCBAF operates under civil or administrative proceedings and typically requires a lower burden of proof than criminal forfeiture. It is endorsed by international bodies such as the United Nations Convention Against Corruption (UNCAC), Financial Action Task Force (FATF), and the World Bank’s StAR Initiative.

Although the Philippines does not yet have a standalone NCBAF statute, its legal framework allows for similar asset recovery mechanisms through Republic Act No. 9160 (Anti-Money Laundering Act of 2001, as amended) and Republic Act No. 1379 (Forfeiture Law)). Under RA 9160, the Anti-Money Laundering Council (AMLC) may freeze assets upon a finding of probable cause, even before a criminal conviction. RA 1379 allows the forfeiture of unlawfully acquired property through civil proceedings, provided the respondent cannot justify the asset’s lawful origin.

In practice, NCBAF-style enforcement has been applied in high-profile cases, such as the 2025 flood control scandal, where the AMLC froze hundreds of bank accounts and properties linked to suspected corruption without waiting for criminal trials. Clearly, Philippine lawmakers should institutionalize the NCBAF by enacting a dedicated law that codifies civil forfeiture standards, procedural safeguards, and inter-agency coordination protocols, aligning domestic practice with international best standards.

The NCBAF, as an anti-corruption program, is extremely relevant in the Philippine context since the public focuses heavily on criminal punishment while criminals are able to use stolen resources to evade the law and hide ill-gotten gains, before and during corruption cases, which typically take five years or more to process (high-profile cases take eight years or more).

Inherent Risks

The problem with the Philippine legal system is that it lacks a dedicated NCBAF law. This means that asset recovery efforts in the Philippines are legally vulnerable. Freezing bank accounts or seizing properties without criminal conviction may be challenged in court for violating due process, especially if they rely solely on administrative discretion. This undermines the legitimacy of enforcement agencies and risks judicial reversals that could discourage future recovery efforts. Moreover, the absence of codified standards creates inconsistency across institutions; agencies may apply asset recovery tools unevenly, leading to procedural bottlenecks and fragmented enforcement. NCBAF legislation will strengthen government institutions, a definite improvement over the highly politicized, all-too-common remedy for corruption cases by administrative discretion.

International cooperation also suffers when domestic laws lack clarity. Foreign jurisdictions often require well-defined legal mandates before honoring asset recovery requests or providing mutual legal assistance. Without a codified NCBAF framework, the Philippines may face delays or denials in repatriating offshore assets, particularly in cases involving complex transnational corruption. This weakens the country’s position in global anti-corruption networks and limits its ability to act swiftly when illicit wealth is moved abroad.

Domestically, the lack of NCBAF legislation means missed opportunities for timely restitution. Criminal trials in the Philippines can take years, during which stolen assets may be dissipated or concealed. A civil forfeiture mechanism would allow the government to act more quickly, preserving public resources and reinforcing public trust. Codifying the NCBAF would send a strong signal of institutional commitment to justice, transparency, and international best practice—ensuring that corruption is not only punished but economically reversed.

Valuation in Asset Recovery

Valuation plays a critical and often underappreciated role in asset recovery programs, serving as a bridge between legal enforcement and economic restitution. At its core, valuation determines the real-world worth of assets linked to corruption, whether they are bank accounts, real estate, corporate shares, luxury goods, or infrastructure contracts. Without accurate valuation, governments risk underestimating the scale of illicit enrichment or overcommitting resources to recover assets with a limited fiscal impact. How many resources should be committed to asset recovery for a given asset with value X? Asset recovery efforts should yield results that surpass the competitive rate of return.

This focus on the return on invested resources is mirrored in other corruption cases. In civil forfeiture and NCBAF proceedings, valuation informs strategic decisions: which assets to prioritize, how to structure settlements, and whether to pursue repatriation across borders. It also supports proportionality in enforcement, ensuring that the value of seized assets aligns with the alleged harm or public loss. Forensic valuation techniques, including discounted cash flow analysis, market benchmarking, and scenario modeling, are especially vital when dealing with shell companies, undervalued landholdings or manipulated procurement contracts.

Moreover, valuation enhances transparency and public trust. When recovered assets are clearly quantified and contextualized—say, a ₱200 million mansion linked to a ₱2 billion flood control scam—the public can better grasp the impact of corruption and the value of recovery. This narrative power reinforces legitimacy, strengthens civic engagement, and pressures political elites to support reforms. In short, valuation is not just a technical input— it is a strategic tool for justice, accountability, and economic repair.

Recoverable Value

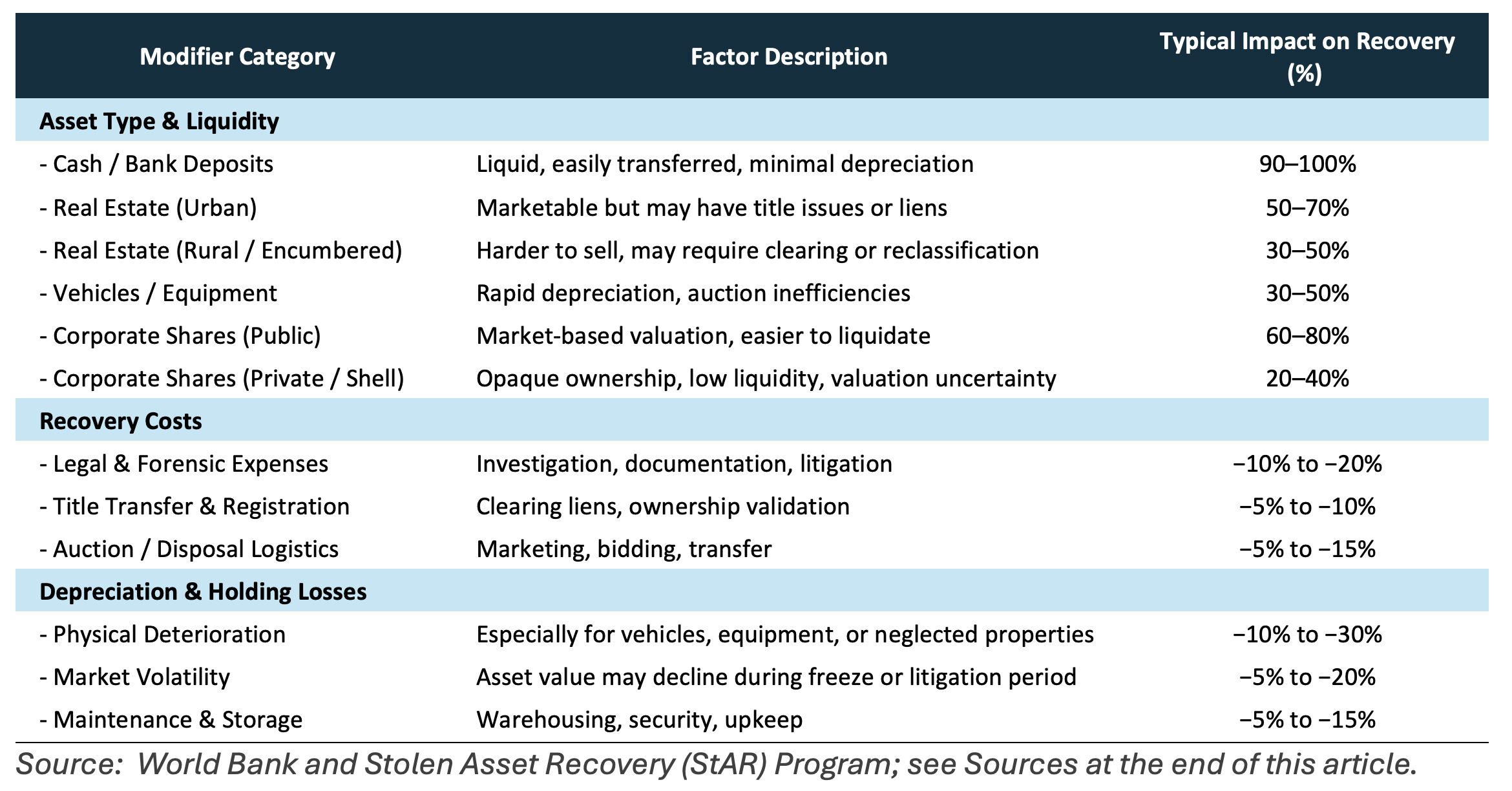

However, what value can be recovered under an asset recovery program such as the NCBAF? In the Philippines, the actual percentage of value recovered varies widely depending on the nature of the asset, the cost of enforcement, and the time it takes to dispose of or repurpose the asset. While the NCBAF offers a faster route to reclaiming illicit wealth compared to criminal forfeiture, it is not immune to friction. Recovery is almost never full; instead, the government may recoup between 30% and 70% of the original transaction value. This range reflects the complex realities of asset tracing, legal processing, and market conversion.

Asset type and liquidity are the first major recovery factors that impact the recoverable value under the NCBAF. Cash and bank deposits are the most straightforward, often recoverable at near full value, minus administrative costs. Real estate, vehicles, and corporate shares are less liquid and may incur substantial recovery costs. Properties may be encumbered, depreciated, or difficult to auction, while vehicles and equipment lose value quickly and incur storage costs. This may explain the large discounts when the Bureau of Customs disposes of smuggled exotic cars caught in ports. And then there are shares in private or shell companies that are hard to value or liquidate, especially if ownership structures are opaque or contested.

Recovery costs further reduce the net returns. These include forensic investigations, legal documentation, title clearing, and auction logistics, among others. In some cases, the government must spend significantly to secure, maintain, and transfer the ownership of seized assets. Holding costs, such as depreciation, maintenance, and market volatility, compound the challenge, especially when assets are frozen for years before disposition. Without competent valuation and strategic prioritization, enforcement agencies risk pursuing assets that cost more to recover than they return to the Filipino people. Thus, valuation is not just a technical input; it is a fiscal safeguard and a strategic compass.

Recoverable Value Factors

The table above enumerates the possible losses in value when recovering ill-gotten assets. However, a 100% value recovery rate is not feasible. However, this outcome is far superior to what has been historically recovered in previous corruption cases. Although valuation is a necessary tool in the NCBAF, its use requires a solid policy foundation to be effective.

Policy Implications

Asset-oriented justice frameworks, such as the NCBAF, offer governments a pragmatic tool for reclaiming illicit wealth without waiting for criminal convictions. In the Philippines, the 2025 flood control scandal demonstrated the NCBAF’s operational viability when the AMLC froze hundreds of assets linked to irregular infrastructure contracts. These civil enforcement actions not only expedited recovery but also signaled a shift toward financial redress and deterrence. Criminals are less likely to attempt to steal government resources if they understand that they will not be able to keep their ill-gotten spoils, even if they are able to forestall judicial punishment. To ensure this certainty, lawmakers must codify the NCBAF through a dedicated statute that defines procedural safeguards, evidentiary thresholds, and inter-agency protocols aligned with international standards.

On the other hand, effective asset recovery depends on more than legal innovation—it requires institutional strength and coordination. Fragmented enforcement, limited forensic capacity, and political interference often hinder progress. The Senate’s “Philippines Under Water” investigation into ₱545.6 billion in flood mitigation projects revealed ghost contracts and contractor monopolies, underscoring the need for specialized teams and forensic integration in the procurement process. Competent, standards-based valuation practices are equally critical. This ensures that recovered assets are accurately assessed, strategically prioritized, and economically meaningful, transforming asset seizure into fiscal repair rather than symbolic punishment.

Moreover, international cooperation remains essential, especially in cases involving offshore accounts and transnational shell entities. Historical efforts to recover Marcos-era wealth illustrate the limitations of slow and fragmented legal coordination. Streamlining mutual legal assistance treaties and adopting flexible multilateral mechanisms would enable faster asset-tracing and repatriation. Meanwhile, technology—digital forensics, AI analytics, and blockchain registries—can enhance transparency and accelerate enforcement of laws. The AMLC’s 2025 freeze operation relies on transaction mapping and inter-agency data sharing, pointing to the promise of tech-enabled recovery when paired with valuation benchmarks.

Finally, anti-corruption policies must confront political and economic realities. The same flood control scandal revealed how only 15 contractors cornered ₱100 billion in public funds, sparking public outrage and forcing an institutional response. Sustained reform requires civic engagement, whistle-blower protection, and visible restitution. Asset recovery must be transparent, valuation-informed, and politically savvy, anchored in both institutional reform and public trust. Only then can it fulfill its promise as a tool of economic justice for the Filipino people.

___________________________________________

Sources

The following literature, statutes, and data sources were used in the development of this article.

Anti-Money Laundering Council ( (2025). Freeze order on assets linked to flood-control corruption. Retrieved from https://www.amlc.gov.ph

Financial Action Task Force (FATF). (2023). Best practices on beneficial ownership and asset recovery. Paris: FATF/OECD.

OECD. (2004). The OECD Convention on Combating Bribery of Foreign Public Officials in International Business Transactions. Paris: OECD Publishing.

Philippine Center for Investigative Journalism. (2025, September). The Marcos corruption blueprint: Offshore banking and asset tracing. Retrieved from https://pcij.org

Reuter, P., & Truman, E. M. (2004). Chasing dirty money: The fight against money laundering. Washington, DC: Institute for International Economics.

Republic Act No. 9160. (2001). Anti-Money Laundering Act of 2001, as amended by R.A. 9194, R.A. 10167, R.A. 10365, R.A. 10927, and R.A. 11521. Retrieved from https://www.amlc.gov.ph

Republic Act No. 1379. (1955). An Act Declaring Forfeiture in Favor of the State Any Property Found to Have Been Unlawfully Acquired by Any Public Officer or Employee and Providing for the Proceedings Therefor. Retrieved from https://lawphil.net

Rose-Ackerman, S. (1999). Corruption and government: Causes, consequences, and reform. Cambridge, UK: Cambridge University Press.

Stephenson, M. (2011). A legal framework for non-conviction based asset forfeiture. World Bank Legal Working Paper Series. Retrieved from https://star.worldbank.org

Transparency International. (2007). Global corruption report: Corruption and the legal profession. London: Routledge.

United Nations Office on Drugs and Crime & World Bank. (2011). Stolen Asset Recovery (StAR) Initiative: Barriers to asset recovery. Washington, DC: World Bank Publications.

Images in this article were generated by AI image generating tools.