The food and beverage (F&B) industry stands as a cornerstone of the global economy, encompassing a wide spectrum of businesses ranging from restaurants and cafes to food processing companies and beverage manufacturers. Its essence lies in its diversity and dynamic nature, continually shaped by the ever-evolving landscape of consumer preferences, technological innovations, and economic factors. Beyond merely providing sustenance, the F&B sector plays a pivotal role in nurturing cultural identity and fostering social interaction on a global scale.

In the Philippines, the F&B industry holds particular significance, reflecting the nation’s rich culinary heritage and vibrant food culture. It serves as a driving force behind the economy, making substantial contributions to GDP and employment. Within its bustling markets, a myriad of local and international brands contends for consumer attention, creating a dynamic and competitive marketplace.

Amidst this backdrop, the F&B industry is experiencing profound transformations driven by several key trends. A notable shift towards healthier food options is evident, fueled by a growing consumer demand for products that offer tangible health benefits, such as organic, natural, and plant-based foods. This trend transcends borders, resonating both in the Philippines and globally, prompting companies to introduce innovative product lines tailored to health-conscious consumers.

Sustainability has emerged as a pressing concern for both consumers and businesses alike, shaping operational practices and marketing strategies within the F&B sector. From sustainable sourcing to the adoption of eco-friendly packaging, a heightened emphasis on environmental responsibility is reshaping industry norms and driving positive change.

The pursuit of convenience is driving significant growth in ready-to-eat meals, meal kits, and food delivery services, spurred on by the proliferation of online food delivery platforms. Technological advancements, ranging from automated kitchens to AI-driven inventory management systems, are revolutionizing operations within the F&B industry, enhancing efficiency and elevating customer engagement.

Moreover, there is a growing appreciation for local and authentic flavors, both domestically in the Philippines and internationally. Traditional Filipino dishes and locally sourced ingredients are experiencing a resurgence in popularity, mirroring a broader global movement towards regional cuisines and artisanal products.

In the aftermath of the COVID-19 pandemic, consumers are increasingly prioritizing foods and beverages that bolster immunity and promote overall health. Ingredients such as turmeric, ginger, and probiotics have surged in demand, reflecting a heightened awareness of wellness and self-care in dietary choices.

In essence, the F&B industry is undergoing a significant evolution, shaped by evolving consumer preferences, technological advancements, and societal shifts. As it navigates these changes, the industry continues to serve as a beacon of innovation and cultural expression, enriching lives and communities worldwide.

Valuation

Valuing companies in the F&B industry involves several key methodologies. One popular approach is the Income Approach, particularly the Discounted Cash Flow (DCF) Methodology. This method estimates the future cash flows of an F&B business and then discounts them back to their present value using a discount rate that captures industry-specific risks. It’s particularly effective for established F&B giants with stable cash flows, like major restaurant chains and beverage producers. The DCF is the standard methodology for business valuations in both the Philippine Valuation Standards, or PVS, and the International Valuation Standards, or IVS.

Another common method is the Market Approach, featuring Multiples-Based Valuation techniques. Here, the company’s Enterprise Value is determined by applying a multiplier to its Earnings Before Interest, Tax, Depreciation, and Amortization (EBITDA). This approach shines when comparing an F&B business to similar publicly traded companies or recent sales of comparable businesses, such as big-name food or beverage brand acquisitions. While easy to use and in common usage, this method is mainly used as a sanity-check on the more technical DCF method.

Meanwhile, the Asset-Based Approach offers another perspective, valuing an F&B company based on the cost of replacing its assets or the potential value from selling them. This includes methods like Replacement Cost or Liquidation Value and is typically used for companies with significant tangible assets, such as food processing plants or large manufacturing facilities. It is particularly relevant for businesses heavily invested in physical infrastructure and equipment. This method is often applied to businesses that are in financial distress that have negative cash flows or due for liquidation.

Quick Case Study

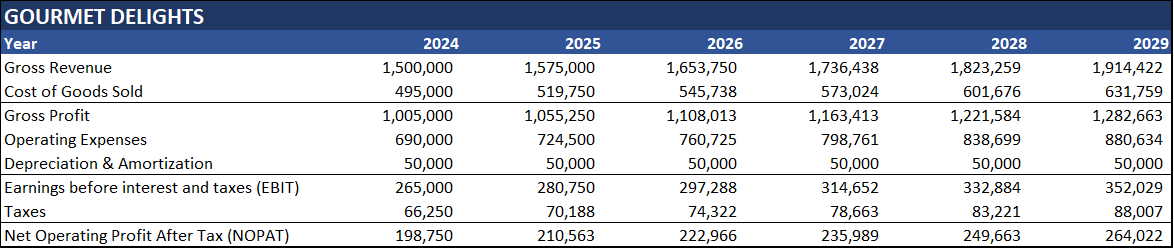

To illustrate valuation methodologies for F&B companies, we’ll delve into a case study featuring a hypothetical entity, Gourmet Delights. Nestled strategically within a vibrant urban landscape, Gourmet Delights operates as a mid-sized restaurant and catering service, capitalizing on three primary revenue streams: dine-in sales, takeaway transactions, and catering services. Projections for revenue are crafted by multiplying the average price per meal or catering order by the anticipated sales volume within specific timeframes.

Here’s a breakdown of the 2024 revenue streams:

| Revenue Streams |

Price per Unit |

Volume per Month |

| Dine-in Sales |

$15 |

6,000 |

| Takeaway Sales |

$10 |

3,000 |

| Catering Services |

$500 |

10 |

To ensure operational efficiency and financial stability, Gourmet Delights follows a meticulous cost framework covering expenses related to ingredients, packaging, rent, utilities, salaries, insurance, and marketing. By effectively managing costs and prioritizing the delivery of top-notch culinary experiences, Gourmet Delights aspires to become the preferred choice for culinary enthusiasts seeking exceptional dining and catering services in the urban landscape.

To further streamline our discussion, let’s establish the following assumptions:

|

Assumptions |

Value |

| Discount Rate (WACC) |

10% |

| Growth Rate |

3% |

| Tax Rate |

25% |

| Annual Revenue Growth |

5% |

|

COGS (% of Revenue) |

33% |

| Operating Expenses (% of Revenue) |

46% |

| Depreciation & Amortization |

$50,000 |

| Capital Expenditures |

$50,000 |

| Change in Working Capital (% of Revenue) |

2% |

With this information, we’re equipped to apply the Income Approach using the Discounted Cash Flow Analysis. The financial model will simulate revenues and cost first.

The revenue projection for the first year are determined by first calculating the monthly revenues, achieved by multiplying the price per unit by the volume per month. Subsequently, the annual revenue is derived by multiplying the monthly revenues by 12, representing the number of months in a year. Adding these annual revenues together yields the total revenue for the first year.

|

Revenue Streams |

Price per Unit | Volume per Month | Monthly Revenue |

Annual Revenue |

| Dine-in Sales |

$15 |

6,000 | $90,000 |

$1,080,000 |

| Takeaway Sales |

$10 |

3,000 | $30,000 |

$360,000 |

| Catering Services |

$500 |

10 | $5,000 |

$60,000 |

| Total Revenue | $125,000 |

$1,500,000 |

Now, let’s proceed to construct the complete DCF projections using the assumptions we outlined earlier. Here’s a step-by-step breakdown of how we’ll conduct the discounted cash flow (DCF) analysis:

1.Project an Income Statement:

-

- The income statement forecasts the company’s financial performance over the next five years, outlining revenue, expenses, and profitability based on earlier assumptions. It serves as the cornerstone for estimating future cash flows, including the calculation of Net Operating Profit After Tax (NOPAT).

2. Forecast Free Cash Flows (FCF):

-

- Free Cash Flow (FCF) is a critical metric in valuation, representing the cash generated by a company’s operations after accounting for necessary capital expenditures. It’s a key indicator of a company’s ability to generate cash for its investors.

- Calculate FCF for each year using the formula:

FCF = NOPAT + Depreciation & Amortization – Change in Working Capital – CapEx

3. Discount the Forecast Free Cash Flows:

-

- Apply a discount rate, typically the Weighted Average Cost of Capital (WACC), to discount the projected FCF. This accounts for the time value of money and the risk associated with the company’s operations.

- Use the provided Present Value Factor (PVF) to discount the forecasted FCF, multiplying each FCF by its respective PVF to derive the discounted FCF for each year.

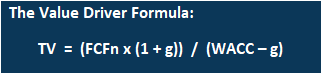

4. Calculate Terminal Value (TV):

-

-

- The Terminal Value represents the value of the company at the end of the forecast period when explicit projections cease. It captures all cash flows beyond the forecast period and is usually estimated using a value driver formula or an exit multiple method.

- In this analysis, calculate the Terminal Value using the value driver formula, assuming a perpetuity growth rate (g) and a constant WACC or discount rate. This reflects the company’s long-term earning potential.

-

-

-

- The provided terminal value is $3,321,501.

-

5. Discount Terminal Value:

-

-

-

- Similar to the forecasted cash flows, discount the Terminal Value to its present value using the same discount rate (WACC) applied to the forecasted cash flows. This ensures that the Terminal Value is expressed in present value terms, reflecting its value as of the valuation date.

- The present value of the terminal value is calculated to be: 2,062,391

-

-

6. Calculate Total Enterprise Value (TEV):

-

-

-

-

- Sum the present values of the discounted forecasted cash flows and the discounted Terminal Value to obtain the Total Enterprise Value (TEV). TEV represents the total value of the company’s operations, accounting for both its near-term cash flows and its long-term earning potential.

- TEV = $2,062,391 + $3,321,501 = $2,987,849.

-

-

-

Following these steps will allow us to conduct a comprehensive DCF analysis, providing valuable insights into the company’s valuation for informed decision-making.

We can leverage the information provided above to explore the Market Approach through multiples-based valuation. In this method, we utilize multiples of key financial metrics to gauge the company’s value relative to industry standards. Specifically, we’ll employ an EBITDA multiple of 8x, which is an average within the F&B industry.

By applying this multiple to the company’s EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), we can estimate its enterprise value. This approach allows us to benchmark the company’s performance against industry peers and assess its valuation in a market context.

Multiples-Based Valuation Using EBITDA Multiple of 8x:

|

Item |

Value |

| EBITDA (2029) |

$402,029 |

| EBITDA Multiple |

8x |

| Terminal Value |

$3,216,230 |

| Sum of Discounted FCFs |

$925,458 |

| Total Enterprise Value |

$4,141,687 |

By multiplying the EBITDA for 2029 by the chosen multiple of 8x, we arrive at the estimated enterprise value of $3,216,230. Additionally, the sum of discounted free cash flows (FCFs) amounts to $925,458. Combining these values yields a total enterprise value of $4,141,687. This method provides an alternative perspective on the company’s valuation, complementing the insights gained from the discounted cash flow analysis.

This method provides an alternative perspective on the company’s valuation, complementing the insights gained from the discounted cash flow analysis. For an F&B compan, this approach is particularly significant as it aligns the valuation with industry standards and expectations. It offers a comparative analysis against peers in the market, providing valuable context on how the restaurant stands in terms of financial performance and market positioning. This highly valuable when evaluating the company’s relative market value, operational efficiency, and profitability compared to similar businesses in the industry.

Now to illustrate the third final approach which is the Asset Based approach, consider the below balance sheet of Gourmet Delights for the year 2024.

|

Balance Sheet |

2024 |

| Assets: | |

| Cash |

$ 150,000.00 |

| Accounts Receivable |

$ 250,000.00 |

| Inventory |

$ 400,000.00 |

| Property, Plant, and Equipment (PPE) |

$ 2,000,000.00 |

| Intangible Assets |

$ 300,000.00 |

| Total Asset Value |

$ 3,100,000.00 |

| Liabilities: | |

| Accounts Payable |

$ 200,000.00 |

| Short-term Debt |

$ 150,000.00 |

| Long-term Debt |

$ 1,000,000.00 |

| Total Liabilities |

$ 1,350,000.00 |

To apply the Liquidation Value Approach to the hypothetical F&B company, we need to determine the value of its assets and liabilities. First, we calculate the Net Liquidation Value by subtracting the total liabilities from the total asset value, resulting in a Net Liquidation Value of $1,750,000.

|

Item |

Value |

| Total Asset Value |

$ 3,100,000.00 |

| Total Liabilities |

$ 1,350,000.00 |

| Net Liquidation Value |

$ 1,750,000.00 |

Next, we assume the assets will be sold at a discount due to liquidation. Applying a 30% discount factor (0.7) for a rapid sale, we adjust the Net Liquidation Value accordingly. This results in a Discounted Liquidation Value of $1,225,000.

| Item | Value |

| Net Liquidation Value |

$ 1,750,000.00 |

| Discount Factor (Optional) |

0.70 |

| Discounted Liquidation Value |

$ 1,225,000.00 |

This reflects the estimated value if the company were to be liquidated and its assets sold off quickly. For an F&B company restaurant, this valuation method is significant because it provides a conservative estimate of the company’s worth in a worst-case scenario. It highlights the minimum value the company’s tangible and intangible assets could fetch if it had to close down and sell its assets rapidly. This approach is significant for stakeholders and potential investors to understand the underlying asset value of the company, ensuring they have a clear picture of the financial safety net provided by the company’s assets.

Some Major Factors to Consider

Several factors can significantly impact the valuation of an F&B company. These include:

- Quality of Earnings: Higher earnings typically lead to higher valuation multiples, reflecting the company’s ability to generate consistent and reliable profits.

- Size: Larger businesses with diversified products and services and a low-risk profile tend to have higher valuations due to their ability to withstand market fluctuations and economic cycles.

- Control Premium: This refers to the additional benefits derived from the ability to control operational and financial policies of the business, often resulting in higher valuations.

- Economy: The state of the economy can significantly impact business valuations. Economic growth generally leads to higher consumer spending and better business performance.

- Age of the Business: Older, more established businesses may have a higher valuation due to their proven track record and established customer base.

Leveraging on these diverse valuation methodologies, stakeholders can gain a well-rounded understanding of an F&B company’s worth, aiding in investment decisions, mergers and acquisitions, and strategic planning in this ever-evolving sector.

Conclusion

To wrap up, valuing companies in the food and beverage sector involves a nuanced process shaped by various factors defining their worth. Beyond financial metrics, this evaluation delves into the complexities of consumer behaviors, market dynamics, and operational efficiencies.

Fundamentally, assessing F&B businesses demands a thorough understanding of industry-specific elements. In a landscape influenced by evolving consumer preferences, regulatory frameworks, and technological advancements, valuation methodologies must adapt to encompass factors such as sustainability, health trends, and technological innovations.

Furthermore, F&B valuation delves into various aspects of operations like production efficiency, distribution networks, and brand recognition. These elements serve as vital determinants, impacting profitability and resilience against market fluctuations.

In navigating this intricate terrain, stakeholders utilize diverse valuation methods, each offering unique insights into company valuation. By integrating income, market, and asset-based approaches, stakeholders gain a comprehensive understanding, blending quantitative analysis with qualitative considerations.

Ultimately, a robust valuation framework serves as a guiding force for strategic decision-making in the F&B industry. Whether guiding investment strategies, facilitating mergers and acquisitions, or shaping long-term plans, an accurate valuation acts as a guiding force, charting the path for sustainable growth and success in this dynamic sector.

Written By: Raccey Baluyot

Aviso Valuation and Advisory Corp. is a real estate consultancy firm that offers valuation and business advisory services that are compliant with international standards such as the International Valuation Standards (IVS) and International Financial Reporting Standards (IFRS). To assure that we only produce high-quality deliverables, as needed, we do tasks beyond the usual appraisal process like verifying pertinent property documents (i.e. land titles, tax declarations, etc.) with the appropriate government agencies for due diligence purposes prior to the acquisition of the properties.