Since its initial transmission in Q1 2020, COVID-19 has had a profound impact on our society. Health and hygiene awareness rose among Filipinos as the risk of infection became ever-present. Importation, preservation, and distribution of vaccines became a matter of utmost importance as the struggle to inhibit the spread of the disease continued. People became more accustomed to working from home and relying on food deliveries as their communities were placed under quarantine. Meanwhile, consumer preferences on food items shifted as more people opted to take stock of products with long shelf lives, particularly those that were either canned, chilled, frozen, or otherwise preserved.

On the other hand, the pandemic took a significant toll on the overall economy as many businesses limited their operations due to recurrent lockdowns and stringent health protocols. For many small and medium firms, the struggle for survival became ever more desperate as a result of limited demand and supply shortages.

Despite this, a few firms saw success in this dilemma by serving the shifting needs of our changing society and adapting their operations to better cater to new emerging trends. One such example is the cold storage industry, which initially saw a catalytic growth in government demand as refrigerated warehouses became more critical for the preservation of vaccines and other pharmaceuticals. As more Filipinos became immunized, however, the prosperity generated by the immunization drive steadily diminished.

Despite this, demand was gradually picked up by the e-commerce industry, which facilitated food deliveries from online groceries. As more consumers favored preserved food items and relied more on online deliveries, food & beverage companies engaged in the e-commerce sector turned to storage firms to prolong the quality of temperature-sensitive products. This renewed the demand for refrigerated units and sustained the sector’s growth.

As 2022 comes to an end and new opportunities appear, the cold storage industry is expected to show further growth as consumer tastes continue to gravitate towards products that require refrigeration for preservation. More so, with the return of pedestrian traffic in metropolitan areas, the sector will see heightened demand not just from online groceries but also from traditional commercial outlets, such as supermarkets and hypermarkets. Facilitating this growth is the completion of vital infrastructure projects that will expand and upgrade our country’s road network, resulting in the improvement of cold chain logistics.

What are Cold Storage facilities?

Cold storage facilities are industrial infrastructures designed to store perishable items and other temperature-sensitive products under controlled conditions in the pursuit of prolonging the shelf life of such commodities.

Competition in the Cold Storage Market

In November 2019, the Cold Chain Association of the Philippines reported 151 cold storage warehouses (CSWs) that were authorized by the Department of Agriculture. Most of these facilities are located on the island of Luzon, which accounts for 82.5% of the accredited facilities. Metro Manila has the highest share of approximately 37.5% (45) of the total warehouses. On the other hand, Central Luzon and CALABARZON each comprise roughly 25% (30) and 20% (24) of the overall supply.

Outside Luzon, the remaining facilities are concentrated in the regions of Davao and Central Visayas, which account for 10.8% (13) and 6.7% (8) of the total, respectively.

Meanwhile, competition in the industry is fierce, with Jentec Storage, Glacier Megafridge, Mets Logistics, Royal Cargo, and Big Blue Logistics dominating the market in terms of cold storage pallets. Aside from these firms, other major players such as Polar Bear Freezing and Storage Corporation, Igloo Supply Chain Philippines, Vifel Ice Plant and Cold Storage, Koldstor Center Philippines, Inc., and Subzero Ice and Cold Storage all vie for a larger share of the market.

They achieve this through a variety of means, such as the implementation of new management strategies, the adoption of novel technologies, and the execution of marketing techniques that increase their competitive edge over their rivals.

Some companies opt to increase their advantage through process automation and AI management systems. Meanwhile, a few construct their facilities near major urban centers or large-scale food production centers in order to increase their logistical efficiency. Some, on the other hand, intensify their marketing campaigns by engaging with their clients either through social media, face-to-face meetings, or a combination of both. Others partner with international brands in an effort to increase their capacity through the conversion of standard warehouses, the modernization of existing facilities, or the development of new ones. However, most of them seek to gain an advantage by either offering their clients flexible rent agreements, more value-adding services or relatively lower rental prices than their immediate competition.

Major Clients of the Cold Storage Industry

Primary demand drivers of the cold storage market are food companies that use the vast majority of refrigerated warehouse to stock raw meat, processed meat, locally dressed poultry, seafood, fruits, and vegetables, as well as a selection of other items such as cakes, frozen dough, ice cream, beverages, dairy products, etc. In several provinces, a substantial percentage of the industry is used for the preservation of raw ingredients for quick-service restaurants (QSRs).

The facility’s location and the local industries it serves determine the demand for refrigerated warehouses. Meat accounts for the majority of the nationwide demand, followed by poultry and then seafood. Meanwhile, fresh produce, dairy products, and other products account for the remaining demand.

Lease Rates of Refrigerated Warehouses

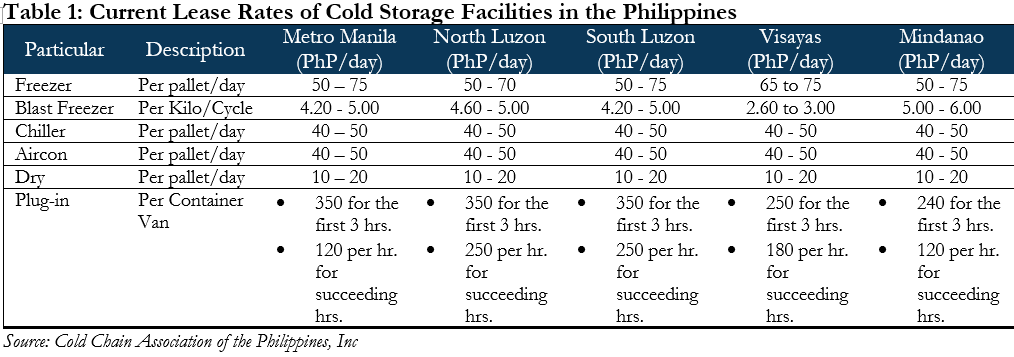

Table 1 summarizes the current lease rates of cold storage facilities in the Philippines. Regardless of the region, the rates of chillers, air-conditioned units, and dry storage units are all the same with respect to each particular category. Meanwhile, the rates of blast freezers in Luzon were relatively similar, ranging from PhP 4.20 per Kilo per Cycle to PhP 5.00 per Kilo per Cycle, with North Luzon having a slightly higher lower rate limit than South Luzon and Metro Manila.

On the other hand, compared to Luzon, Visayas has the lowest price range for blast freezer units, while Mindanao has the highest.

When it comes to freezers, most regions have shown comparable rates, which range from PhP 50 per pallet per day to PhP 75 per pallet per day. However, Visayas and North Luzon have slightly different rate limits than the rest.

Meanwhile, Plug-in units are relatively more expensive in the regions of Luzon and cheapest in Mindanao.

Allowable Load Limit Per Pallet

According to the Cold Chain Association of the Philippines, low temperature conditions inside refrigerated warehouses affect the material integrity and useful life of plastic pallets, therefore, the pallets cannot be loaded at full capacity (1 to 1.2 tons). Despite this, the allowable load limit per pallet varies depending on the perishable commodity. Table 2 presents the allowable load per pallet for commodities that require cold storage for preservation. A typical plastic pallet can only carry 300 to 400 kg of whole chickens and processed meats, while boxed fish are allowed a slightly higher range of 500 to 600 kg.

Meanwhile, boxed beef, pork, and poultry are provided with the highest limits of 600 to 800 kg per pallet. The data presented in the table may indicate that products contained in cardboard boxes are allowed heavier loads than those packaged in plastics, probably because they can be more neatly and tightly packed on top of the pallets. In addition, the facility may not have to provide plastic/metal containers in order to neatly store their client’s plastic-enclosed products, thereby eliminating the need to place further unnecessary weight on top of the pallets.

Inbound and Outbound Cargo Expenditures

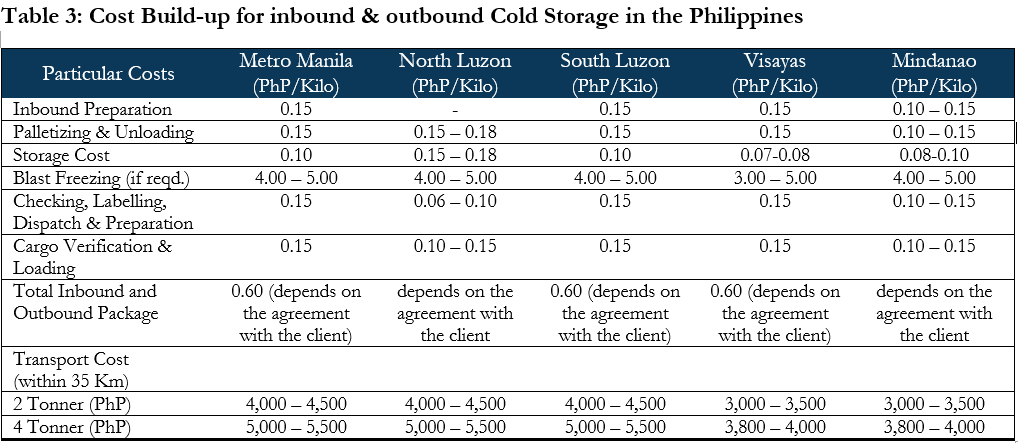

Generally, cold storage firms offer a package deal that includes all the costs associated with receiving and shipping commodities to and from their facilities. According to the Cold Chain Association of the Philippines, these deals typically cost a total of Php 0.60 per kilo. However, the pricing can vary depending on the client’s agreement with the storage firm.

Table 3 highlights that the cost accumulation for incoming and outgoing commodities to and from a refrigerated warehouse is broadly comparable across all regions of Luzon, with North Luzon having slightly higher inbound costs but slightly lower outbound costs compared to South Luzon and Metro Manila. However, despite this, the former has lower outbound costs relative to the other two regions in Luzon.

Meanwhile, inbound and outbound costs in Visayas and Mindanao are comparable to those of the northern islands. However, the attractiveness of Mindanao’s facilities in the refrigeration market is arguably the greatest among the three island groups, as they can offer cheaper rates to both current and prospective clients.

Aside from inbound and outbound costs, storage costs notably vary between them, as Visayas reportedly has the lowest prices, while Luzon has the highest. Moreover, transport costs in Luzon are significantly higher than in Visayas and Mindanao.

Demand and Growth Drivers of the Cold Storage Market Sector

In 2021, the sudden and rapid transmission of the COVID-19 virus drastically increased the number of infected cases in the Philippines. In response, the national government appealed to foreign nations for more vaccine donations. However, when the beneficence arrived, the government found itself lacking the necessary infrastructure to store the vaccines, maintain their efficacy, and facilitate their distribution. As a result, the government urged warehouse firms to expand their cold storage infrastructure in order to address this dilemma. As the number of infected cases rose and more vaccines arrived, the importance of refrigerated warehouses in the government’s efforts to restrict infections became more evident, and the state’s demand for more facilities increased, thus sparking the growth of the cold storage market.

Aside from the national government, the expansion of the industry was catalytically driven by the online grocery market, which experienced unprecedented growth as demand for online food items, such as frozen foods, perishable food products, processed food stuffs, and convenience store meals increased due to the recurrent implementation of lockdowns and community quarantines.

As Filipinos acclimate to the “new” normal conditions, post-pandemic e-commerce growth and storage demand for food, beverages, frozen food products and perishable food items may contribute to a somewhat slower but more sustainable, long-term growth of the sector. Aside from this, other factors are expected to contribute to its post-pandemic growth. These include the following:

- Urbanization

- Population growth

- Food consumption

- Busy lifestyle of consumers

- Consumer-driven economy

- Preference for timely deliveries

- Economic recovery and growth

- Exportation of fruits and vegetables

- Client specific value-adding services

- Vertical integration of supply chains

- Warehouse expansion and modernization

- Health concerns over food quality and safety

- Rise of end-to-end supply chain logistics integration

- Ascendance of the e-commerce sector and online shopping

- Continued nationwide administration of COVID-19 vaccinations

- Improvement of infrastructure developments that favor cold chain logistics

- Integration of new technologies in the development of new facilities & improvement of current ones

- Shifting consumption patterns from homemade meals to dine-outs, take-outs, food deliveries and roaming food hawkers

- Shifting food preference to desserts, cold beverages, frozen food commodities, and ready-to-eat convenience store meals.

- Changing grocery shopping patterns from local wet and dry markets to hypermarkets, supermarkets, and online grocery shopping

- Construction of new, automated cold chain facilities with large storage capacities, fully automated processes, artificial intelligence systems, and sophisticated software managed solutions.

- Consistent mass production, importation, and consumption of perishable food products (raw meat, poultry, seafood, fruits, and vegetables), processed food items (dairy, desserts, nuggets, and sausages), and pharmaceutical products (vaccines, insulin, and Botox).

Although the cold storage sector has witnessed significant growth over the previous years, the construction of investment-grade facilities remains a lucrative investment area in the country as it remains under-resourced. At present, the limited availability of refrigerated warehouses is insufficient to fulfill the growing demand for such facilities. However, as the economy recovers from the pandemic, the expansion of the industry is expected to continue as it gradually satisfies the demand through the development of new infrastructure. In the future, consolidation of the industry is expected as a result of mergers between local and international firms that seek to satisfy their clients’ specific requirements through the utilization of advanced technological innovations, competitive management strategies, and high-volume storage facilities.

Challenges that Inhibit the Growth of the Cold Chain Industry.

Despite the country’s growing demand for cold storage market, the industry is currently confronting difficulties that will influence corporate decisions for both investment planning and operations management. These issues include the following.

- High costs in utilities

- Seasonal demand for produce

- Inconsistent annual crop yields

- A byzantine government bureaucracy

- Deficiency of independent cold storage operators

- Limited capacity due to insufficient storage facilities

- Unintegrated transport system and inefficient logistics industry

- High investment requirements due to high startup expenditures

- Outdated cold storage facilities that fail to meet modern standards

- Recurrent electricity disruptions as a result of irregularities in power supply

- A fragmented, highly competitive market dominated by a few major players

- High operating costs, miscellaneous costs and other unexpected expenditures

- The absence of end-to-end management and integration of supply chain logistics

- High lease rates due to a limited number of modern refrigerated warehouse spaces

- Remote location of food producing regions that inhibit efficient transport logistics.

- Frequent occurrence of extreme weather conditions, such as droughts and typhoons

- Inadequate infrastructure developments, such as ports, highways, bridges and shipping lanes

- Inefficient distribution of international and domestic shipping throughout the country’s major shipping transport hubs, such ports and harbors.

- The inability of obsolete warehouses to maintain freezing point conditions for extended periods of time or under unexpected power interruptions.

- The incapacity of transportation vehicles to sustain low temperature conditions over long distances and prolonged traffic disruptions.

Despite the problems that were mentioned previously, it is expected that the cold storage industry will continue to exhibit growth in the future as these issues are addressed and demand continues to intensify. The sector is poised for rapid development as a number of infrastructure projects initiated by the previous administration are well underway toward completion. Meanwhile, the supply of modern facilities is increasing as both new (FAST Logistics and AC Logistics Holdings Corp.) and old (Glacier Megafridge Inc.) players are constructing new warehouses in different regions of the country. In addition, the supply is further bolstered as some companies endeavor to expand their operations, either through the renovation and expansion of existing infrastructure or through the modification and conversion of standard warehouses into refrigerated facilities. High floor load capacity, and ceiling heights are desired in order to maximize warehouse volume.

On the other hand, major market players, such as Royal Cargo Storage Inc., aim to increase their competitive edge by upgrading existing facilities through the adoption of technical innovations, such as artificial intelligence, operation automation, and warehouse software management solutions, in order to digitize, optimize, and streamline their operations. In contrast, some firms opt to provide more value-added services and adopt efficient management strategies in order to increase their competitiveness in the market.

Written By Kevin Kyle B. Santos

Aviso Valuation and Advisory Corp. is a real estate consultancy firm that offers valuation and business advisory services compliant to international standards such as the International Valuation Standards (IVS) and International Financial Reporting Standards (IFRS). To assure that we only produce high-quality deliverables, as needed, we do tasks beyond the usual appraisal process like verifying pertinent property documents (i.e. land titles, tax declarations, etc.) with the appropriate government agencies for due diligence purposes prior to the acquisition of the properties.

_________________________________________