Written By: Mary Grace C. Ladringan

Tourism remains one of Southeast Asia’s most powerful engines of inclusive growth, generating employment, foreign exchange, and regional integration. Yet within this dynamic landscape, the Philippines continues to underperform relative to its neighbors.

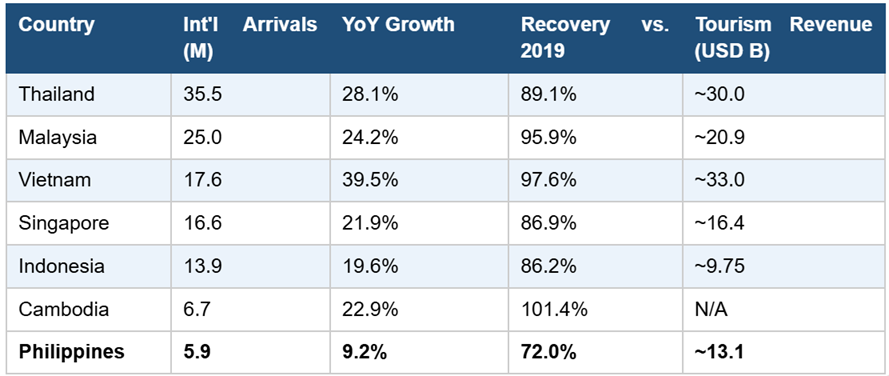

In 2024, Southeast Asia’s six major tourism markets welcomed 121.3 million international arrivals, but the distribution highlights a widening competitiveness gap. The Philippines received 5.9 million arrivals, below its 7.7 million target and only 72% of its 2019 level. In contrast, Vietnam saw 17.6 million visitors, a 39.5% increase that nearly restored pre-pandemic numbers. Thailand and Malaysia recorded 35.5 million and 25.0 million arrivals, respectively. The Philippines’ 9.2% growth rate was the lowest in the region.

The pattern has persisted into 2026. The Department of Tourism reported 2.74 million international visitor arrivals from January to May, rising to roughly 2.96 million by mid-June — a year-on-year increase of about 7.5 percent that keeps the country on a path toward its revised, and more modest, full-year target of 6.7 million. That target itself reflects the scale of the gap: it was set after the Philippines missed its 2024 goal of 7.7 million (closing at 5.9 million) and its 2025 goal of 8.4 million (closing at roughly 5.6 million), while Thailand has set a 2026 target of 36.7 million and Vietnam 25 million. Even on an improving trajectory, the Philippines’ 2026 pace remains well below its own 2019 peak of 8.26 million arrivals, let alone the volumes now routine among its regional peers.

The gap is not primarily one of attractiveness. The Philippines boasts more than 7,600 islands, consistently top-ranked beaches such as El Nido and Siargao, and exceptional marine biodiversity. Rather, as researchers at the Philippine Institute for Development Studies (PIDS) concluded in a landmark 2026 sectoral review, the country is underperforming because of weak systems—specifically, the infrastructure and connectivity frameworks that determine whether interest translates into actual arrivals.

Table 1: Southeast Asia Tourism Performance, 2024

Sources: ASEANstats (2024); Outbox Company Southeast Asia Tourism Recap (2025); The International Investor (2025).

The Infrastructure Advantage: Regional Comparators

Phu Quoc airport Vietnam

The correlation between transport infrastructure investment and visitor arrivals is well-documented across Southeast Asia. Thailand’s Suvarnabhumi and Don Mueang airports together handled over 100 million passengers annually pre-pandemic, supported by a domestic aviation network reaching every major tourist hub. Vietnam invested aggressively in airport capacity expansion in the early 2020s, adding international terminals in Phu Quoc, Can Tho, and Van Don, directly unlocking new tourism corridors. Malaysia’s multi-gateway strategy—with Kuala Lumpur, Penang, Johor Bahru, and Kota Kinabalu all serving international routes—distributes arrivals and reduces dependency on a single hub.

Laos offers perhaps the most striking recent case study: the opening of the Laos-China Railway in 2021 directly drove a surge in Chinese arrivals to Vang Vieng and Luang Prabang, contributing to more than USD 1 billion in tourism revenue in 2024 and demonstrating how targeted infrastructure investment can rapidly convert latent demand into economic output.

As Dr. Maria Cherry Lyn Rodolfo of the Asian Institute of Management argued at a 2026 PIDS webinar, connectivity policy is in effect tourism policy. In an archipelago where virtually all international visitors arrive by air, and domestic movement relies on a combination of air and sea travel, the performance of the tourism system is determined by its weakest link.

The Philippine Infrastructure Constraint

Airport Capacity and Saturation

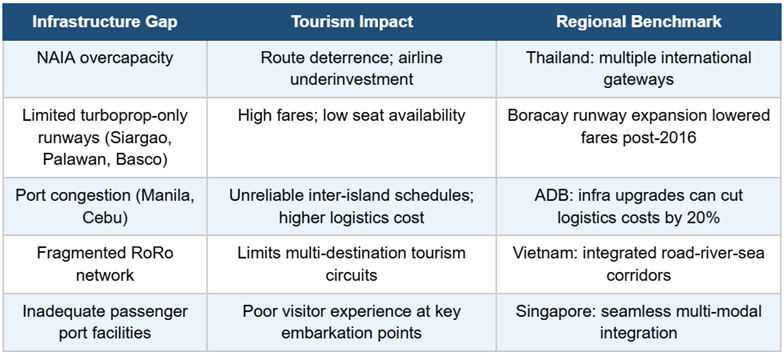

The Ninoy Aquino International Airport (NAIA), the country’s primary international gateway, has long operated beyond its rated capacity of approximately 35 million passengers per year—a condition that directly deters airline investment, limits route expansion, and creates operational bottlenecks that affect the visitor experience from arrival. While the New Manila International Airport (NMIA) in Bulacan is projected to address this constraint upon completion, its development timeline remains a critical variable in near-term tourism competitiveness.

PIDS Senior Research Fellow Dr. John Paolo Rivera identified limited airport capacity as among the most binding structural bottlenecks constraining Philippine tourism, alongside high travel costs, weak inter-island connectivity, and investment friction. The consequence is measurable: the Philippines attracted only 484,465 intra-ASEAN visitors in 2024, against Malaysia’s 17.9 million and Thailand’s 10.8 million—figures that reflect not only marketing gaps but structural access barriers.

The High Cost of Flying to Philippine Destinations

Perhaps no issue more viscerally captures the accessibility problem than domestic airfares to the Philippines’ own premier tourist destinations. In 2025, round-trip flights from Manila to Siargao—a two-hour journey—reached PHP 25,000 to PHP 30,000, prompting the Department of Transportation (DOTr) to formally summon airlines for inquiry. For context, comparable international trips to Japan, Thailand, or Vietnam were frequently available at lower prices.

The structural driver is infrastructure, not solely pricing behavior. Siargao’s Sayak Airport operates with a runway length that restricts access to smaller turboprop aircraft. These planes carry far fewer passengers, distributing fixed costs—fuel, crew, maintenance, airport fees—across a smaller seat count, which structurally elevates per-seat fares. The Department of Tourism’s Secretary Christina Garcia-Frasco noted that Siargao, Palawan, and Basco remain largely dependent on turboprop aircraft, which constrains seat supply and pushes fares higher.

The Boracay precedent is instructive: runway extension in 2016 at Caticlan’s Godofredo P. Ramos Airport permitted larger jet aircraft to land, immediately increasing seat supply and driving airfares down. This experience confirms that infrastructure investment, not regulation alone, is the durable solution to domestic airfare accessibility.

The commercial impact has been acute. In 2025, Camarines Sur Representative Nelson Legacion stated before Congress that for many Filipino families, a flight-and-hotel package to a nearby Asian destination is now cheaper than flying to domestic islands. Philippine Airlines subsequently agreed to cap one-way Siargao fares at PHP 11,000—still above its stated route average of PHP 7,500 to PHP 8,000—underscoring the persistence of structural cost pressures.

Sources: DOTr public statements (August 2025); Philippine Star (August 2025); Manila Bulletin (February 2026); market fare comparisons.

Seaport Deficiencies and Passenger Ferry Infrastructure

For an archipelago of over 7,600 islands, sea transport is not a secondary mode—it is a primary means of domestic tourism mobility. Yet Philippine seaports face compounding structural constraints. The Port of Manila, the country’s busiest, is chronically congested, with vessels regularly queueing outside the port awaiting berth space. A 2016 study by the Philippine Institute for Development Studies (PIDS) specifically identified port congestion as a major transport and logistics challenge requiring infrastructure investment.

For tourism, port deficiencies translate into unreliable inter-island travel, extended journey times, and deterrence for multi-destination itineraries. Tourists planning to combine Palawan with the Visayas, or Siargao with Surigao’s canyons, face a fragmented transport network where scheduling unreliability is a known risk. The Asian Development Bank (ADB) has noted that improving transport infrastructure can reduce logistics costs by as much as 20%—a figure that, applied to tourism circuits, would directly lower the total cost of multi-destination trips and extend average visitor length of stay.

The Philippines operates approximately 120 seaports nationally, but the distribution, condition, and passenger facility quality of these ports is uneven. Many ports serving tourism destinations lack adequate passenger terminals, ticketing systems, and connecting road access—creating friction at precisely the point where visitor experience is formed. The absence of roll-on/roll-off (RoRo) route optimization further limits the development of integrated land-sea tourism corridors across regions such as the Visayas and Mindanao.

Tourism as a System, Not a Sector

The dominant policy discourse around Philippine tourism has often centered on marketing spend, branding campaigns, and destination promotion. Yet the data suggest that demand is not the primary constraint. The Philippines recorded more than 134 million domestic tourist trips in 2024—the highest in Southeast Asia—generating USD 63.4 billion in domestic tourism spending and accounting for 35.8% of ASEAN’s total domestic tourism expenditure. This reflects both strong domestic demand and the resilience of Filipino travelers.

What domestic dominance also reveals is that international conversion—the rate at which global interest translates into actual arrivals—is weak. The Philippines’ return on tourism investment (RoTI) has been estimated at approximately USD 0.57 per dollar invested, against Vietnam’s estimated USD 1.94 and Thailand’s consistently above USD 1.50. The gap reflects not weak assets but weak systems—the connectivity, logistics, and service networks that transform destination appeal into visitor flows.

PIDS research is explicit on this point: we are underperforming not because of weak potential, but because of weak systems. The implication for infrastructure investment is direct. Every peso invested in runway extension, passenger port modernization, or domestic route development carries measurable tourism multiplier effects—longer stays, higher per-visitor spend, and broader geographic distribution of economic benefits beyond the three or four historically dominant destinations.

Sources: PIDS Discussion Paper (2025); ADB transport assessments; DOT and DOTr public reports.

Emerging Investment Opportunities

The Philippines’ infrastructure pipeline contains several high-leverage projects that could meaningfully shift its tourism competitiveness trajectory. The New Manila International Airport in Bulacan, when fully operational, will add substantial gateway capacity and reduce congestion-driven deterrence. Airport modernization programs in Cebu, Davao, and Clark expand the multi-gateway model that has proven effective in Malaysia and Thailand. Expressway extensions connecting Clark and the Subic Bay Freeport area to Metro Manila improve surface access for the Central Luzon tourism corridor, encompassing Bataan’s heritage sites, the Zambales coast, and Pampanga’s culinary and cultural offerings.

The Visayas and Mindanao present the highest long-term upside, given their concentration of underdeveloped but world-class natural assets. Realizing this potential requires the sequencing of infrastructure investments—runway upgrades, passenger port modernization, and RoRo network expansion—that reduce the cost and friction of inter-island movement. The PIDS sectoral review is explicit that reforms cannot be pursued simultaneously across all fronts; prioritization aligned with visitor movement patterns and demonstrated demand corridors is essential to ensuring capital generates measurable returns.

Public-private partnerships (PPPs) remain the most viable mechanism for accelerating tourism-supporting infrastructure at the scale and pace required. The Philippine government’s Build Better More program identifies transport infrastructure as a national priority, and ADB continues to support Philippines connectivity projects. Aligning these investments with tourism demand modeling—identifying where infrastructure gaps most directly constrain conversion from interest to arrival—is a precondition for maximizing economic impact.

Conclusion

The Philippines does not lack tourism assets. What it lacks is the infrastructure that makes those assets accessible—consistently, affordably, and at scale. The data are unambiguous: a 72% recovery rate against pre-pandemic arrivals, in a region where neighbors have reached or exceeded 2019 levels; a domestic airfare to Siargao that rivals the cost of flying to Tokyo; seaports that struggle to deliver the reliability and passenger experience that multi-destination tourism requires.

The challenge is not demand—it is systems. Closing the tourism competitiveness gap with ASEAN peers requires treating infrastructure investment as tourism investment: runway extensions that unlock jet service and lower fares, passenger port modernization that enables reliable inter-island itineraries, and gateway diversification that distributes arrivals beyond the Manila bottleneck.

The opportunity cost of inaction is measurable. Vietnam’s RoTI of approximately USD 1.94, achieved in part through deliberate connectivity investment, versus the Philippines’ USD 0.57, represents not a marketing gap but an infrastructure efficiency gap. Addressing it—through strategic, sequenced, and demand-aligned investment—is the most direct path to unlocking the Philippines’ considerable tourism potential.

Tourism Begins with Connectivity

At Aviso Valuation & Advisory Corp., we recognize that transport infrastructure, strategic site selection, and feasibility planning play a vital role in unlocking tourism potential. Understanding how people move, where investments should be located, and how destinations can be made more accessible is essential to creating sustainable tourism growth and long-term economic value.

Our advisory practice integrates infrastructure demand analysis, tourism corridor mapping, and site feasibility assessment to support developers, investors, and public-sector partners in making evidence-based location and investment decisions.

___________________________________________________________________

References

Asian Development Bank (ADB). Philippines transport and connectivity assessments. www.adb.org/where-we-work/philippines

Asian Development Bank Institute (ADBI). Serrona, K. et al. (2021). Sustainable Tourism: The Case of the Siargao Islands in the Southern Philippines. ADBI Working Paper 1302.

ASEAN Statistics Division (ASEANstats). (2024). Visitor Arrival Statistics to ASEAN Member States. data.aseanstats.org

Department of Tourism, Philippines. (2024–2025). Official tourism arrival statistics and press briefings.

Department of Transportation (DOTr), Philippines. (August 2025). Statement on Siargao airfare investigation. Reported in Philippine Star, August 19, 2025.

Manila Bulletin. (August 2025). Siargao airfares: Why this flight costs more than a trip to Tokyo. mb.com.ph

Manila Bulletin. (February 2026). DOT seeks airfare reforms amid rising cost of domestic travel. mb.com.ph

Outbox Company. (March 2025). Southeast Asia Tourism Performance 2024 Recap. the-outbox.com

Philippine Institute for Development Studies (PIDS). (March 2026). Strong demand, but structural challenges constrain PH tourism growth. Press Release PR1326. pids.gov.ph

Philippine Institute for Development Studies (PIDS). Rivera, J.P. et al. (2025). Philippine Tourism Sectoral Review (2000–2025): From Promise to Power. PIDS Discussion Paper 2025-43.

Philippine Institute for Development Studies (PIDS). Patalinghug, E. et al. (2016). Easing Port Congestion and Other Transport and Logistics Issues.

Philippine Institute for Development Studies (PIDS). (2024). Transport Infrastructure in the Philippines: From Plans to Impact. PIDS Discussion Paper 2024-51.

Tribune. (January 2026). Siargao flight fares cut amid tourism concerns. tribune.net.ph

BusinessWorld. (September 2023). Closing gaps in infrastructure prescribed to address lagging tourism recovery. bworldonline.com

Panao, R.A. (February 2026). Philippines lags ASEAN in tourism rebound. Analysis via Inquirer/Asian News Network. asianews.network / globalnation.inquirer.net

The Diplomat. (August 2025). Southeast Asia’s Uneven Tourism Recovery, Explained. thediplomat.com

The International Investor. (June 2025). Policy Report: Which Southeast Asian Countries Truly Profit from Tourism. theinternationalinvestor.substack.com

World Bank. (2009). Philippines: Transport for Growth—An Institutional Assessment of Transport Infrastructure.