A trilateral partnership among the United States, Japan, and the Philippines is reshaping Luzon’s economic geography — and with it, the landscape for real estate, infrastructure finance, and professional advisory services.

By Angelo M. Gandia

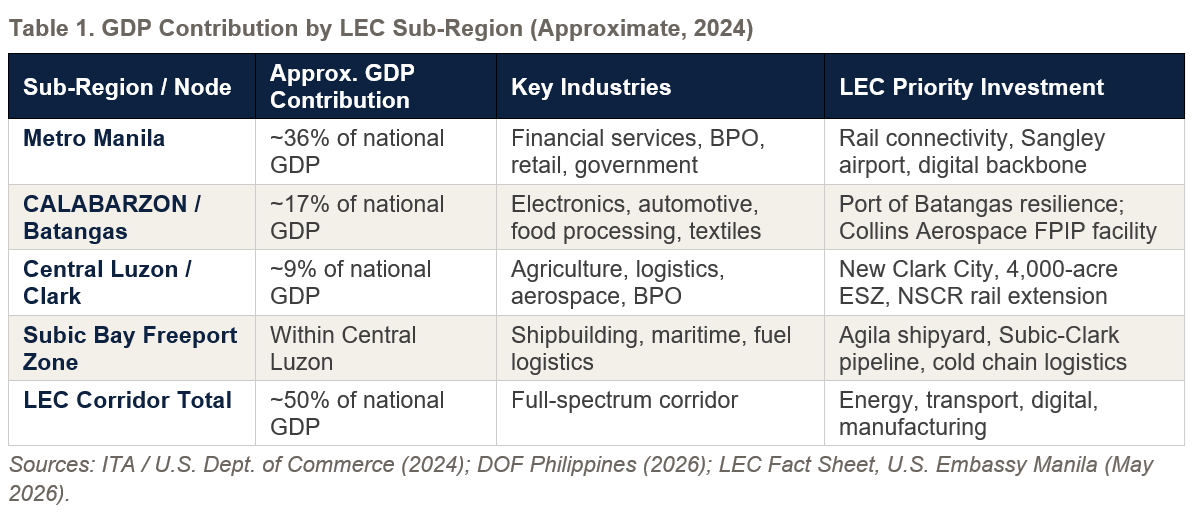

The Luzon Economic Corridor (LEC) is the inaugural Indo-Pacific economic corridor under the Partnership for Global Infrastructure and Investment (PGI), jointly established by the United States, Japan, and the Philippines in April 2024 and expanded in May 2026 to include eight additional partner nations. Anchored on the quadrilateral nodes of Subic Bay, Clark, Metro Manila, and Batangas, the LEC encompasses the Philippines’ dominant economic zone — contributing approximately 50 percent of national GDP. This article provides a data-driven analysis of the corridor’s macroeconomic, regional, and sectoral impacts, with particular attention to the real estate sector.

The proclamation of the Luzon Economic Corridor at the first United States-Japan-Philippines Trilateral Leaders’ Summit in April 2024 marked a structural inflection point in Philippine economic development policy. More than a bilateral aid arrangement, the LEC operates as a multilateral investment coordination framework — mobilizing public and private capital across energy, transport, digital infrastructure, and advanced manufacturing.

As of May 2026, the LEC Steering Committee convened its inaugural session, formally welcoming Australia, Canada, Denmark, France, Italy, the Republic of Korea, Sweden, and the United Kingdom as partner nations.¹ The initiative now encompasses eleven countries and a growing roster of private sector entities, from U.S. private equity firm I Squared Capital to Korean conglomerate HD Hyundai and U.S. aerospace manufacturer Collins Aerospace.

“The corridor will strengthen supply chain security and resilience in key sectors, transforming Luzon into a more prosperous and interconnected region while delivering value to foreign partners and investors.”

— LEC Fact Sheet, U.S. Embassy Manila / DOF Philippines, May 2026

The economic rationale is compelling. The LEC corridor — spanning Metro Manila (~36% of national GDP), CALABARZON/Batangas (~17%), and Central Luzon (~9%) — collectively represents the Philippines’ primary productive engine.² Accelerating connectivity, energy security, and digital infrastructure across this corridor carries outsized multiplier effects for the broader Philippine economy and its ~115 million population.

LEC’s Impact on the Philippine Economy

GDP and Investment

With the corridor accounting for approximately half of Philippine GDP, even marginal improvements in logistics efficiency, energy cost, and digital connectivity translate into measurable national output gains. The Philippine economy registered GDP growth of 4.0% in Q3 2025, a deceleration from 5.5% in Q2 2025, partly attributable to infrastructure spending uncertainties and typhoon disruptions.³ The IMF subsequently revised its 2025 growth forecast to 5.1%. Against this backdrop, the LEC’s coordinated capital injection represents a countercyclical stimulus with long-duration productivity effects.

The business environment reforms enacted concurrently with LEC are structurally significant. The CREATE MORE Act extends up to 40 years of fiscal and non-fiscal incentives. The Investors’ Lease Act extends land lease terms to 99 years. The Accelerated Right-of-Way (ARROW) Act — historically the single largest bottleneck for Philippine infrastructure — streamlines land acquisition. The Capital Markets Efficiency Act reduces the stock transaction tax from 0.6% to 0.1%, aligning the Philippines with regional peers.⁴

Employment and Labor Market

The LEC’s infrastructure investments are expected to generate significant demand in construction and manufacturing — sectors with high labor multipliers. The Philippines’ unemployment rate stood at 4.0% in April 2024, down from 4.5% a year earlier, with 48.36 million employed.⁵ The LEC’s emphasis on advanced manufacturing and digital services positions it to upgrade employment quality — not merely quantity — toward higher value-added sectors including BPO, IT, healthcare, and aerospace engineering.

Regional Impacts Along the Corridor

The LEC’s four primary nodes — Subic Bay, Clark, Manila, and Batangas — each present distinct growth dynamics. Corridor economics literature (ADB, 2023) consistently shows that infrastructure-led corridors deliver differentiated spatial effects: nodes nearest to primary logistics hubs experience the earliest and steepest appreciation, while intermediate zones benefit from spillover agglomeration.

Clark and Central Luzon

The Clark Freeport and New Clark City stand as the LEC’s northern manufacturing anchor. The planned 4,000-acre Economic Security Zone — the first AI-native investment acceleration hub under the Pax Silica Initiative — is designed to attract allied manufacturing and semiconductor supply chain tenants.⁴ The North-South Commuter Railway (NSCR), with Japanese ODA financing, will connect Calamba to Clark International Airport, dramatically expanding the effective labor market catchment of Clark’s economic zones.

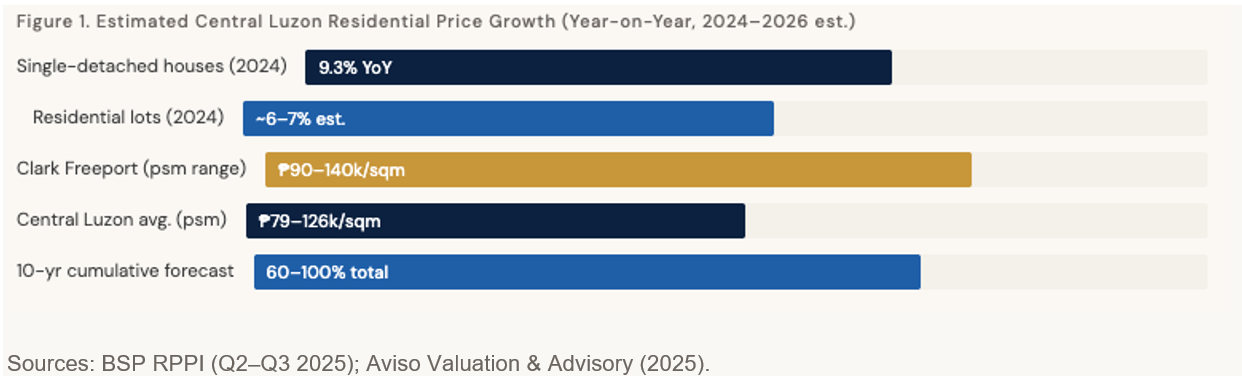

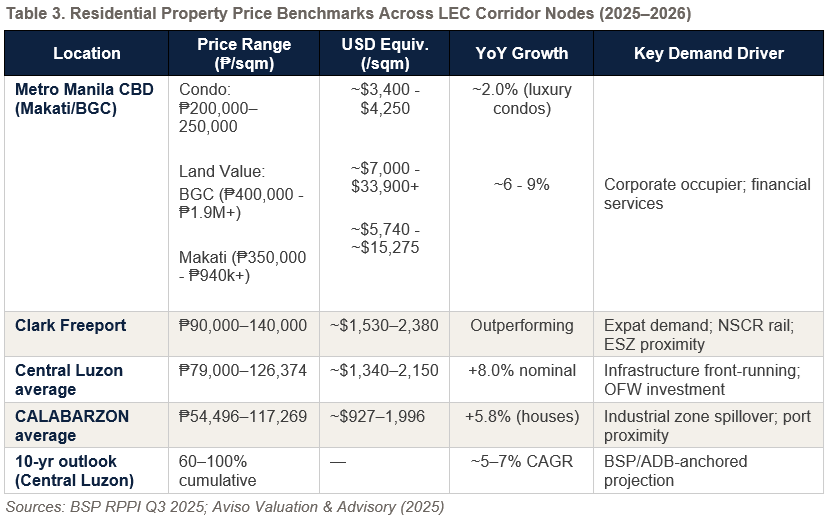

Central Luzon achieved 6.1% GDP growth in 2023, outperforming the national average. Property prices rose approximately 8% nominally in the 12 months to January 2026, with the median home price at approximately ₱4.2 million and the Clark-influenced average at ₱6.5 million.⁶

Subic Bay

Subic Bay’s renaissance under the LEC is driven by maritime, logistics, and energy infrastructure. I Squared Capital’s acquisition of Philippine Coastal Storage & Pipeline Corporation — the largest independent import terminal in the Philippines with a capacity of 6.3 million barrels, housing over 20% of the country’s import storage capacity — anchors Subic Bay’s role as a primary fuel logistics hub.⁴ The proposed 45-mile Subic-Clark fuel pipeline will further integrate the energy supply chain, removing hundreds of fuel trucks from congested regional roads. The Agila Subic Shipyard rehabilitation — via Cerberus Capital Management and HD Hyundai — is reconstituting Philippine shipbuilding capacity.

Batangas and CALABARZON

Batangas, as the LEC’s southern terminus, is positioned for industrial and logistics uplift. Collins Aerospace’s new 7,846 sqm facility at the First Philippine Industrial Park in Santo Tomas, Batangas signals the corridor’s capacity to attract Tier 1 aerospace manufacturers. The Port of Batangas — receiving structured resilience and competitiveness advisory from the U.S. State Department — is slated to become a decongestion node for Port of Manila, with rail integration via the SCMB freight line.⁴

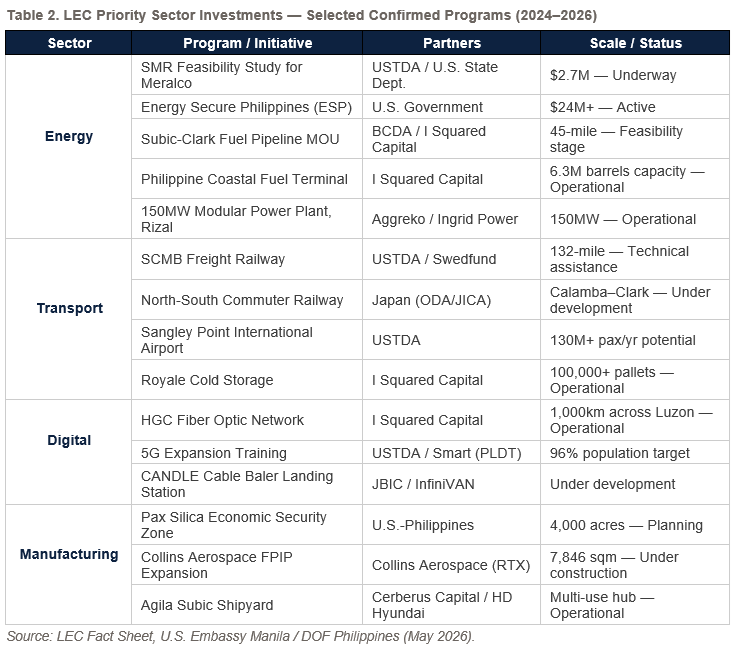

Sectoral Impacts

The LEC operates across four priority investment verticals, each with distinct catalytic mechanisms and multiplier profiles. The following table summarizes key confirmed investments and programs as of May 2026.

Impact on the Real Estate Sector

Infrastructure corridors are among the most potent drivers of real estate value creation. The transmission mechanism — improved connectivity → reduced effective distance → expanded labor and consumer markets → increased land demand → capital appreciation — is well-documented in ADB’s economic corridor development literature. The LEC is generating measurable and forward-priced real estate dynamics across its four nodes.

Market Context

The Philippines real estate market was valued at USD 94.4 billion in 2025 and is projected to reach USD 135.9 billion by 2034 at a CAGR of 4.12%.⁷ Nationwide residential property prices grew just 1.9% year-on-year in Q3 2025 — a sharp deceleration from 9.77% in Q4 2024 — with luxury CBD condominium units in Metro Manila falling 2.04% to PHP 202,590/sqm.³ Metro Manila’s overall office vacancy reached 24.5% in H1 2025, projected to peak at 25.8% by year-end.⁸

Against this nationwide softening, LEC-adjacent corridors — particularly Clark, Pampanga, and Bulacan — demonstrate relative resilience, with infrastructure-expectations-based pricing embedding rail and expressway completion timelines into asset values years ahead of physical completion. The Malolos-Clark Railway alone is projected to add a connectivity premium of 5–15% for well-located properties along its corridor.⁶

Industrial Real Estate

The LEC’s manufacturing orientation is producing structural demand for industrial real estate — warehousing, cold storage, industrial parks, and logistics hubs. The government’s sustained infrastructure investment equivalent to 5–6% of GDP is directly reshaping industrial and logistics hub landscapes in Central Luzon and CALABARZON.⁸ Nearly 1,000 hectares of new industrial and commercial property development is planned in Central Luzon through 2027.⁶ The PEZA network of economic zones remains the institutional backbone for industrial real estate development, offering fiscal incentives that enhance investor returns.

The Importance of Valuation and Transaction Advisory Services

The LEC’s investment architecture — spanning sovereign-backed ODA, development finance, private equity, public-private partnerships, and corporate FDI — creates a complex, multi-layered transaction environment that elevates the demand for rigorous, independent valuation and advisory services to a strategic necessity, not a procedural afterthought.

Why Valuation Matters in Corridor Economics

Economic corridors restructure spatial value distributions rapidly and non-linearly. Properties proximate to rail stations, port upgrades, or industrial estate designations can experience step-change appreciation not captured in historical comparables — the standard basis for market value assessment. Simultaneously, compulsory acquisition under the ARROW Act and right-of-way negotiations for the SCMB Railway and NSCR extensions require defensible, standards-compliant valuations that withstand legal and regulatory scrutiny.

The expanded Investors’ Lease Act — with 99-year lease terms — demands robust leasehold valuation methodology, as income capitalization and DCF models for 99-year ground leases differ materially from standard freehold assessment. Foreign investors unfamiliar with Philippine property law require advisory support in structuring lease agreements, understanding encumbrances, and pricing risk appropriately.

The LEC creates substantial demand for sophisticated valuation and transaction advisory services due to the scale and complexity of the investments involved.

Infrastructure corridors require:

- Land acquisition and right-of-way valuation

- Feasibility studies and highest-and-best-use analyses

- PPP and joint venture structuring

- Financial modeling and investment appraisal

- Market studies and transaction due diligence

Valuation professionals play a critical role in ensuring that projects are economically viable, bankable, and compliant with international standards such as the International Valuation Standards Council framework.

Similarly, transaction advisors are essential in structuring public-private partnerships, attracting institutional investors, and mitigating financial and regulatory risks. As the corridor attracts multinational capital and sovereign-backed infrastructure financing, advisory standards increasingly need to align with global practices used by institutions such as the Asian Development Bank and the World Bank.

Transaction Advisory in a Multilateral FDI Environment

The LEC’s investment roster includes private equity firms (I Squared Capital, Cerberus Capital Management), sovereign-linked entities (JBIC, JICA, USTDA), multilateral development banks (ADB), and corporate majors (Collins Aerospace, Smart Communications). Each brings distinct return expectations, fiduciary standards, and deal structuring requirements. Transaction advisory services — spanning financial due diligence, asset structuring, tax optimization, and cross-border regulatory navigation — are essential intermediaries between capital and deployment.

“Infrastructure investments of this scale restructure spatial value distributions in ways that historical comparables cannot capture. Independent valuation is the analytical foundation upon which defensible investment decisions and equitable public acquisitions rest.”

— — Synthesized from ADB Economic Corridor Guidance Note (2023) and DOF LEC Framework

PPP transactions under the new PPP Code require independent valuations to establish availability payments, equity contributions, and concession fees. The Port of Batangas resilience program, the Sangley Point International Airport development, and the SCMB Railway are all structured as potential PPP vehicles, each demanding multi-scenario financial models, asset valuations, and risk allocation frameworks.

Conclusions and Forward Outlook

The Luzon Economic Corridor is not merely an infrastructure program — it is a structural reordering of the Philippine economy’s spatial geometry, supply chain position, and investment thesis. The corridor’s four nodes, connected by an emerging rail-port-digital spine and energized by coordinated multilateral capital, position the Philippines as a credible Indo-Pacific manufacturing and logistics hub within a decade.

For the Philippine real estate sector, the LEC implies a sustained, infrastructure-led demand cycle — concentrated in industrial, logistics, and residential assets along the Clark–Manila–Batangas axis — even as the broader market navigates near-term headwinds from oversupply and macroeconomic softness. Ten-year price appreciation of 60–100% in Central Luzon is the base scenario, contingent on infrastructure milestone delivery and sustained FDI inflow.

Critically, the efficiency and equity of LEC-linked transactions — from compulsory acquisitions under the ARROW Act to PPP concession pricing and private equity asset deals — depend on rigorous, independent, standards-aligned valuation and advisory services. As the corridor attracts increasingly sophisticated international capital, the demand for Philippine advisory firms capable of bridging local regulatory knowledge with international practice standards will be one of the corridor’s most consequential professional market dynamics.

Aviso Valuation and Advisory Corp. is a real estate consultancy firm that offers valuation and transaction advisory services that are compliant with international standards such as the International Valuation Standards (IVS) and International Financial Reporting Standards (IFRS).

_________________________________________________________________

References

¹ Department of Finance Philippines / U.S. Embassy Manila. (May 2026). LEC Fact Sheet and Trilateral Joint Statement. dof.gov.ph

² International Trade Administration, U.S. Department of Commerce. (2024). Philippines: Luzon Economic Corridor. trade.gov

³ Global Property Guide. (2025). Philippines Residential Property Market Analysis 2026; BSP RPPI Q3 2025.

⁴ U.S. Embassy Manila. (May 2026). Fact Sheet: Luzon Economic Corridor. ph.usembassy.gov

⁵ CCI France Philippines. (June 2024). Luzon Economic Corridor to Boost Investments and Job Creation (citing DOF Sec. Ralph Recto).

⁶ Bamboo Routes. (Jan–Sep 2025). Central Luzon Property Market Analysis, Forecasts, and Housing Prices; BSP RPPI Q2–Q3 2025.

⁷ IMARC Group. (2025). Philippines Real Estate Market Size, Share & Outlook 2034.

⁸ Ayala Land. (Dec 2025). 2026 Philippine Real Estate Market Outlook

⁹ Asian Development Bank. (2023). Economic Corridor Development: Guidance Note. adb.org